Debt Snowball vs. Avalanche: Which Saves You More Money? (With Calculator)

Compare the two most popular debt payoff methods side by side. See exactly how much each strategy costs you in interest and time with real numbers and an interactive calculator.

Founder of Smart Debt Flow. Building transparent debt management tools with AI coaching and BNPL tracking.

The $4,271 Question: Which Strategy Is Right for You?

You have decided to get serious about paying off debt. You have tallied your balances, cut the subscriptions, and found an extra $300 a month to throw at your loans. Now comes the question that splits every personal finance community in half: do you use the Debt Snowball or the Debt Avalanche? The answer matters more than most people realize. Depending on your debt mix, the difference between these two strategies can be $4,000 or more in total interest paid, or six months or more in time to debt freedom. But the "mathematically best" answer is not always the one that works in practice. This guide breaks down both methods with real numbers, explains the psychology behind each, and includes a calculator so you can see the exact difference for your specific situation. No theory. No platitudes. Just the math and the behavioral science you need to make a decision you will stick with.

How the Debt Snowball Works

The Debt Snowball, popularized by Dave Ramsey, is simple: list all your debts from smallest balance to largest, regardless of interest rate. Make minimum payments on everything except the smallest debt. Throw every extra dollar at that smallest balance until it is gone. Then take the total amount you were paying on that debt (minimum plus extra) and add it to the minimum payment on the next-smallest debt. Repeat until everything is paid off. The core mechanic is psychological momentum. When you eliminate a $500 medical bill in two months, your brain registers a win. That dopamine hit reinforces the behavior, making it easier to stay disciplined through the harder months ahead. A 2016 study in the Journal of Consumer Research tracked 6,000 debt holders and found that people who tackled small balances first were significantly more likely to eliminate all their debt than those who prioritized by interest rate. The researchers concluded that the sense of progress from closing accounts was a stronger predictor of success than the financial efficiency of the strategy. The Snowball works best when you have several small debts (under $1,000) alongside larger ones. If you can knock out two or three small balances in the first 60 to 90 days, the momentum becomes self-sustaining. You free up cash flow as minimum payments disappear, and each payoff proves that the system works. The downside is real and measurable: you will pay more in interest. If your smallest debt is a $400 store card at 0% APR and your largest is a $15,000 credit card at 24% APR, the Snowball has you ignoring the most expensive debt first. Over a multi-year payoff, that can cost thousands of extra dollars.

How the Debt Avalanche Works

The Debt Avalanche is the mathematically optimal strategy. List all your debts from highest interest rate to lowest. Make minimum payments on everything except the highest-rate debt. Direct every extra dollar at that most expensive balance first. When it is paid off, roll its payment into the next-highest-rate debt. The logic is straightforward: interest is the cost of carrying debt. By eliminating the most expensive debt first, you minimize the total interest you pay and reach debt freedom faster in most scenarios. If you have a credit card at 24% APR and a car loan at 5% APR, every dollar applied to the credit card saves you roughly five times more in future interest charges than the same dollar applied to the car loan. The Avalanche shines when there is a wide spread between your highest and lowest interest rates. If you are carrying a $12,000 balance at 26% APR alongside a $3,000 personal loan at 8%, the Avalanche saves significant money because it stops the highest-rate interest from compounding for as long as possible. The drawback is psychological. If your highest-rate debt also has your largest balance, you may spend six months or more making payments without the satisfaction of closing an account. For some people, this lack of visible progress leads to discouragement and eventually abandoning the plan entirely. The best strategy in the world is worthless if you quit in month four.

Head-to-Head: A Real-World Comparison

Let us run the numbers on a realistic debt scenario. Imagine you have four debts and $500 per month available for total debt payments (minimums plus extra): Medical bill: $650 balance, 0% APR, $50 minimum payment. Store credit card: $2,100 balance, 21% APR, $63 minimum payment. Personal loan: $5,400 balance, 12% APR, $120 minimum payment. Major credit card: $8,900 balance, 24% APR, $178 minimum payment. Total debt: $17,050. Total minimum payments: $411. Extra payment available: $89 per month. With the Snowball, you pay off the medical bill first (7 months), then the store card, then the personal loan, then the major credit card. Total time to debt free: 41 months. Total interest paid: $6,847. With the Avalanche, you attack the 24% credit card first, then the 21% store card, then the 12% personal loan, then the 0% medical bill. Total time to debt free: 38 months. Total interest paid: $5,692. The Avalanche saves $1,155 in interest and gets you debt free three months sooner. That is real money. But here is the trade-off: with the Snowball, you close your first account in month 7. With the Avalanche, your first account closure does not happen until month 24. That is 17 months of discipline without a single win. For highly motivated, spreadsheet-driven people, those 17 months are fine. For most humans, that is a long time to stay engaged without visible progress. This is why both methods exist and why neither is universally "better."

The Hybrid Approach: Best of Both Worlds

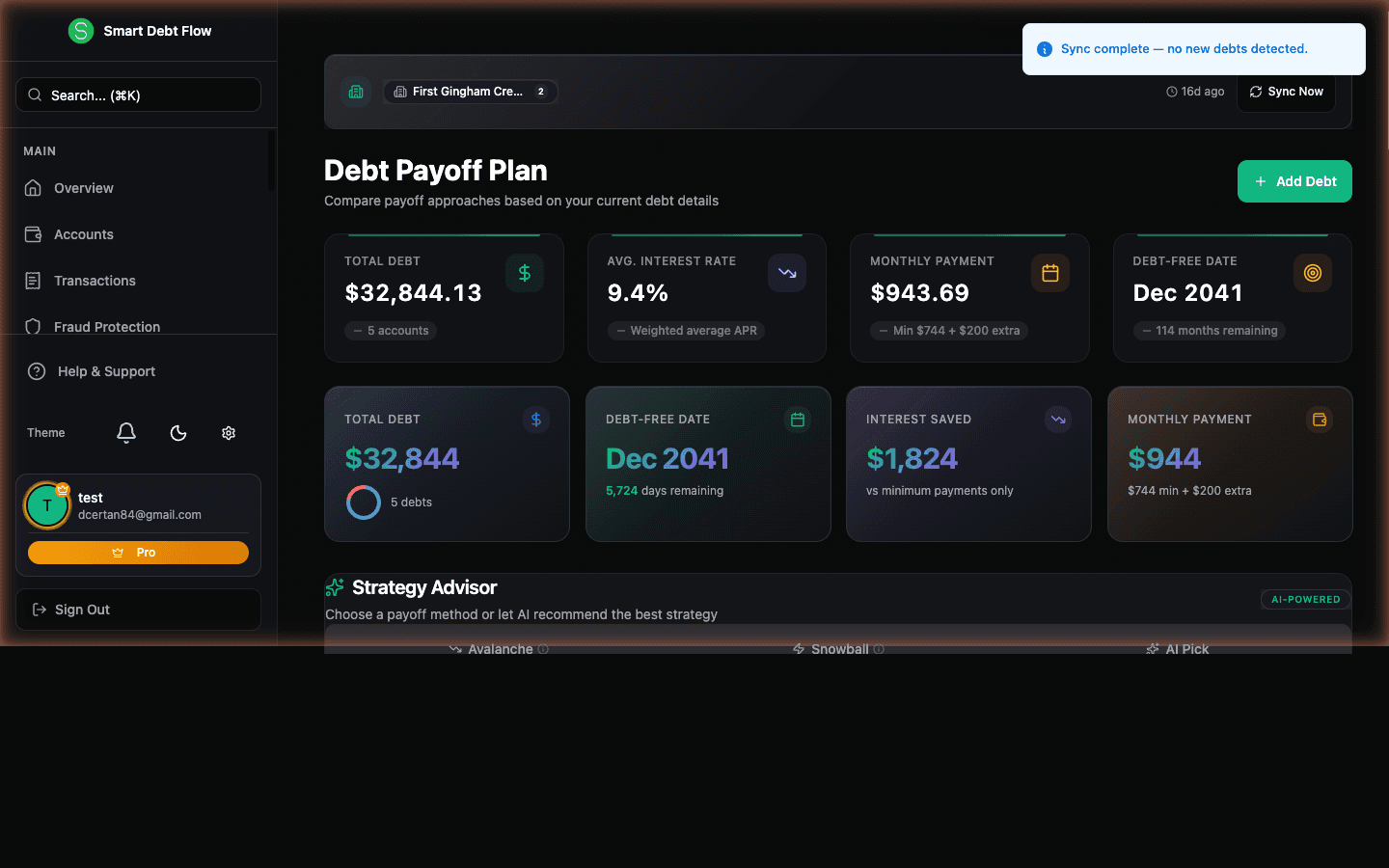

There is a third option that most personal finance advice ignores: start with the Snowball, then switch to the Avalanche. This hybrid approach captures the motivational benefits of quick wins while minimizing the interest penalty. Here is how it works: if you have one or two debts under $1,000 that can be eliminated in 60 to 90 days, pay those off first regardless of their interest rate. The psychological benefit of closing accounts early is worth the small interest cost. Once you have that momentum, switch to the Avalanche and attack your remaining debts in order of interest rate. In the example above, the hybrid approach would pay off the $650 medical bill first (7 months, no interest cost since it is 0% APR), then switch to the Avalanche for the remaining three debts. Total interest paid: $5,710, just $18 more than the pure Avalanche but with the early win of closing an account in month 7 instead of month 24. Smart Debt Flow calculates all three strategies for your specific debts, showing projected payoff dates, total interest, and month-by-month payment schedules. You can see exactly which approach saves you the most money and decide whether the interest difference is worth the motivational trade-off.

Try the Calculator: See Your Numbers

The only way to know which strategy is right for you is to run the math on your actual debts. Our free debt payoff calculator lets you enter each debt with its balance, interest rate, and minimum payment, then compares the Snowball, Avalanche, and Hybrid side by side. You will see your projected debt-free date for each strategy, total interest paid under each method, the month-by-month payment schedule, and how much you save by choosing one over the other. The calculator updates in real time as you adjust your extra monthly payment amount, so you can also see how adding $50 or $100 more per month changes your timeline. Try the free calculator at smartdebtflow.com/debt-calculator, or sign up for Smart Debt Flow to get a full dashboard that tracks your progress, sends payment reminders, and adjusts your plan automatically as you pay down balances.

When the Snowball Beats the Avalanche

Despite being less efficient on paper, the Snowball is often the better choice in several specific situations: You have multiple small debts. If three or four of your debts are under $1,000, the Snowball lets you eliminate them quickly and dramatically simplify your financial life. Going from eight monthly payments to four is a meaningful quality-of-life improvement that also reduces the risk of missed payments. You have a history of starting and stopping. If you have tried to pay off debt before and quit, the Snowball's built-in reward system may be what you need to stay the course. There is no shame in choosing the strategy that you will actually complete. Your interest rates are similar. If your debts range from 15% to 20% APR, the mathematical difference between Snowball and Avalanche is small. In that scenario, choose the Snowball for the motivational benefits without meaningful interest cost. You need cash flow relief. Each small debt you eliminate frees up its minimum payment. If you are living paycheck to paycheck and a single unexpected expense could derail your plan, the Snowball provides faster cash flow relief by reducing your mandatory monthly obligations sooner.

When the Avalanche Is the Clear Winner

The Avalanche is the stronger choice when the math strongly favors it: You have a wide interest rate spread. If your highest-rate debt is at 28% and your lowest is at 4%, every month you delay paying the expensive debt costs you significant money. The Avalanche prevents the most expensive debt from compounding unchecked. Your highest-rate debt has a moderate balance. If your most expensive debt is a $3,000 credit card at 26% APR, the Avalanche lets you eliminate it relatively quickly while saving the most interest. You still get a reasonably quick win. You are disciplined and data-driven. If you track your net worth monthly, maintain a spreadsheet, and find motivation in watching your total interest charges decline, the Avalanche aligns with how your brain already works. You have a long payoff timeline. If your total debt will take three or more years to eliminate, the interest savings from the Avalanche compound over time. A $2,000 difference in year one becomes $3,000 or more by year three because of reduced principal accruing less interest.

The Factor Nobody Talks About: Extra Payments

Here is what matters more than which strategy you choose: how much extra you pay each month. The difference between Snowball and Avalanche is often $1,000 to $3,000 over a multi-year payoff. The difference between paying $100 extra per month and $300 extra per month can be $10,000 or more in interest savings and years off your timeline. In the example above, increasing the extra payment from $89 to $200 per month cuts the Avalanche payoff from 38 months to 29 months and saves an additional $1,800 in interest on top of the strategy savings. That single change has a bigger impact than the choice between Snowball and Avalanche. This is why obsessing over strategy selection is often a form of productive procrastination. The most important step is starting. Pick whichever method resonates with you, then focus your energy on finding more money to throw at your debt. Sell unused items, pick up a side gig, negotiate a raise, cut expenses. An extra $150 per month matters more than which debt you apply it to first. Smart Debt Flow helps you find these extra payment opportunities by analyzing your spending patterns and showing you exactly how each additional dollar accelerates your payoff date. The AI coaching engine identifies specific areas where you can reallocate spending and shows the impact in real time.

Make Your Choice and Start Today

Stop researching. Start paying. The perfect strategy executed tomorrow loses to a good strategy executed today, because every day you wait, interest accrues on every balance you carry. Here is your action plan: First, list every debt with its balance, interest rate, and minimum payment. Second, decide your strategy: Snowball for motivation, Avalanche for savings, or Hybrid for both. Third, set up automatic payments so your extra payment hits your target debt on payday, before you have a chance to spend it elsewhere. Fourth, track your progress monthly, because watching balances decline is the fuel that keeps you going. If you want to skip the spreadsheet and see all three strategies calculated instantly for your specific debts, try Smart Debt Flow free. The app models Snowball, Avalanche, and Hybrid payoff plans, tracks your progress automatically, and adjusts your plan as you make payments. It even factors in your BNPL installments, which most debt trackers miss entirely. The average Smart Debt Flow user identifies their optimal strategy within five minutes of signing up. Whether you choose the Snowball, the Avalanche, or something in between, the only wrong choice is not starting.

RELATED TOPICS

Continue Reading

Ready to Apply What You've Learned?

Use Smart Debt Flow's AI-powered tools to implement these strategies and achieve your financial goals faster.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Financial strategies should be tailored to individual circumstances. Consult with a certified financial planner or advisor for personalized recommendations.

Last Updated: March 21, 2026