Complete Guide to Debt Management Strategies

Learn proven debt management strategies including Snowball and Avalanche methods. Expert advice on choosing the right payoff plan.

Founder of Smart Debt Flow. Building transparent debt management tools with AI coaching and BNPL tracking.

Why a Debt Management Strategy Matters

Carrying debt without a clear repayment plan is one of the most common reasons people stay trapped in a cycle of minimum payments and growing balances. A structured debt management strategy gives you a concrete timeline for becoming debt-free, reduces the total interest you pay, and provides the psychological momentum you need to stay motivated. Many people find that a written payoff plan is easier to follow because it turns a vague goal into specific next steps. The first step is simply choosing an approach and committing to it.

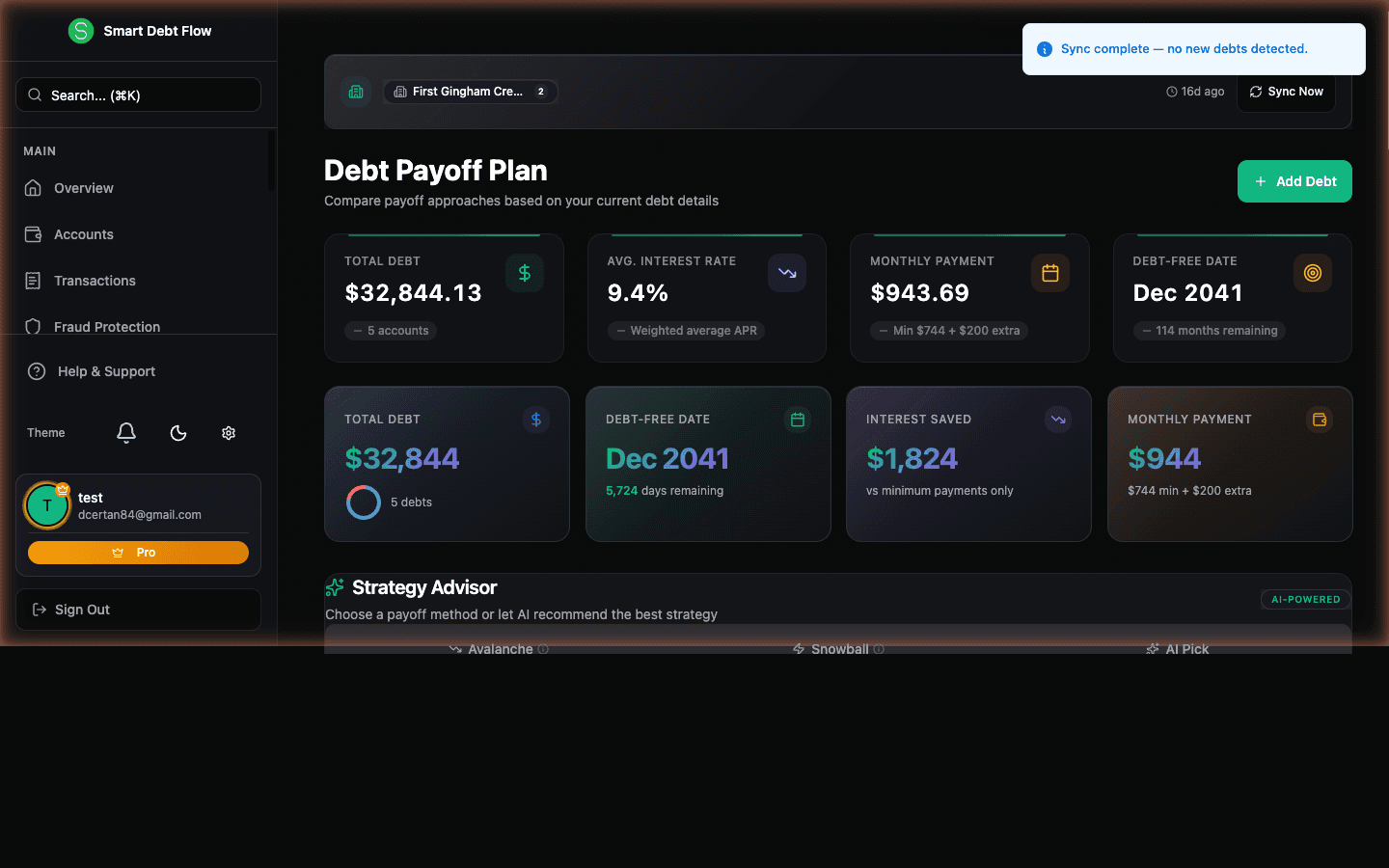

The Debt Snowball Method

Popularized by personal finance educator Dave Ramsey, the Snowball method asks you to list all debts from smallest balance to largest, regardless of interest rate. You make minimum payments on every account and throw every extra dollar at the smallest balance first. Once that debt is gone, you roll its payment into the next-smallest balance. The power of this approach is behavioral: each paid-off account delivers a quick win that reinforces your commitment. A 2016 study published in the Journal of Consumer Research confirmed that people who experienced early successes were significantly more likely to persist in paying off all their debts.

The Debt Avalanche Method

The Avalanche method is the mathematically optimal counterpart to the Snowball. Here you order debts by interest rate from highest to lowest and focus extra payments on the most expensive debt first. By targeting the highest-rate balance, you minimize total interest charges over the life of your repayment plan. For someone with a mix of credit cards at 22% APR and a student loan at 5%, the Avalanche can save thousands of dollars compared to the Snowball. The trade-off is that the highest-rate debt may also have the largest balance, which means it can take longer to score that first payoff milestone.

Choosing the Right Strategy for You

Neither method is universally superior; the best strategy is the one you will actually follow. If you struggle with motivation and need early wins, the Snowball is likely the better fit. If you are disciplined and want to minimize total cost, the Avalanche will save you more money in interest. Some borrowers use a hybrid approach, paying off one or two small debts first for a psychological boost, then switching to the Avalanche order for the remaining balances. Smart Debt Flow can model both strategies with your actual numbers so you can see projected payoff dates and total interest for each path.

Building a Sustainable Repayment Plan

Whichever method you choose, the foundation is a realistic budget that identifies how much extra you can direct toward debt each month. Start by tracking your spending for 30 days, then categorize expenses into needs, wants, and savings. Look for recurring subscriptions you no longer use, negotiate lower rates on insurance or phone plans, and redirect those savings to your debt payoff fund. Automating your extra payments removes the temptation to spend the money elsewhere. Finally, revisit your plan every quarter to adjust for changes in income, expenses, or interest rates.

When to Seek Professional Help

If your total unsecured debt exceeds 40% of your annual gross income, or if you are unable to cover minimum payments, it may be time to consult a nonprofit credit counseling agency. Certified counselors can negotiate lower interest rates through a Debt Management Plan, which consolidates payments into a single monthly amount. Be cautious of for-profit debt settlement companies that charge high fees and can damage your credit score. The National Foundation for Credit Counseling (NFCC) maintains a directory of accredited agencies that offer free or low-cost consultations.

RELATED TOPICS

Continue Reading

Ready to Apply What You've Learned?

Use Smart Debt Flow's AI-powered tools to implement these strategies and achieve your financial goals faster.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Financial strategies should be tailored to individual circumstances. Consult with a certified financial planner or advisor for personalized recommendations.

Last Updated: December 12, 2025